ASEAN Economic Community: In an Uncertain Global Trading Environment

Abstract:

The paper focuses on Association of Southeast Asian Nations (ASEAN) course towards the establishment of an economic community, based on the ASEAN Community Vision 2025. This vision was reiterated by the Foreign Ministers of the ASEAN who met on August 2, 2018, at the 51st ASEAN Foreign Ministers’ Meeting (AMM) in Singapore. At the present juncture the realisation of an ASEAN community continues to be an uphill challenge. From the 1997 Asian Financial Crisis that derailed the region’s strong economic growth trajectory to the current emerging uncertainty in the existing multilateral global trading environment, these persisting economic uncertainties along with the emerging security challenges could undermine its growth and threaten ASEAN’s larger integration process.

Introduction

This year the ASEAN foreign ministers meeting took place at a unique time. On the one hand there are escalating trade-related developments that continue to threaten the multilateral trading regimes, while there has also been an easing of levels of tension in the Korean peninsula with the US-North Korea rapprochement. While the security threat continues to be a major challenge for the region, as it undermines the economic growth and slows down the ASEAN Economic Community (AEC) process. The emphasis across the various meetings was towards further narrowing the developmental gap within ASEAN by deepening economic integration and connectivity. In order to realise this strengthening ASEAN’s centrality and unity would be fundamental especially in a rapidly changing regional and global environment. Thereby, building new as well as renewing old partnerships in mutual areas of traditional and emerging interest. The ministries agreed to identify key trade facilitation initiatives and measures that would contribute to meeting the target of 10% reduction in trade transaction cost by 2020 and doubling intra-ASEAN trade by 2025.1

Singapore’s Prime Minister Lee Hsien Loong, while delivering the inaugural address to the 51st ASEAN Foreign Ministers’ Meeting emphasised on the need for the association to stay on the path of economic integration.2 The concern in the path towards ASEAN’s economic integration as raised by the Singaporean Prime Minster could be attributed to the current pressure faced by the multilateral trading system. Given the uncertainty in the global economic system the leaders at the meeting emphasised on the continued effort towards strengthening collaboration within as well as with its external partners. Under Singapore’s chairmanship the 2018 theme for ASEAN is “resilient and innovative”, signalling the region’s commitment to foster its collective future-readiness. The theme seeks to address both the short and long term aspirations of ASEAN. According to the Secretary General of ASEAN, Dato Lim Jock Hoi, “...Short-term resilience calls for the political will to stay undivided, agility and responsiveness in addressing short-term shock, and innovation in tackling non-traditional issues. While the long-term resilience will call both the ability to embrace and thrive in the new digital age, and to tap into new innovations and technologies to solve common challenges and issues....” According to Mr Hoi, given the current uncertain global economic climate, ASEAN would have to demonstrate its resolve to market openness and support for a rules-based, non-discriminatory multilateral trading system that underpins much of growth and prosperity for decades.3

ASEAN Economic Growth Story

From the 1940s to the 1960s, Southeast Asian nations such as Indonesia, the Philippines, Malaysia, and Singapore began attaining their independence from colonial rule. In their pursuit of nation building these newly independent nations with their ethnically diverse society had to face the twin challenges of economic underdevelopment and maintaining national unity. Southeast Asia changed dramatically during the 1960s and 1970s, which were marked by growing tension as a consequent of a bipolar Cold War world order. The Association of South East Asia (ASEAN) established in 1967 was designed to be a regional alliance for greater regional economic cooperation. ASEAN which was created to manage internal as well as external threat in order to ensure a stable political and economic environment in the region, sought to be a ‘zone of peace, freedom, and neutrality’. As a response, the five founding member-states—Indonesia, Malaysia, Singapore, Thailand, and the Philippines—agreed on a ‘treaty of amity and cooperation’ (TAC) for the peaceful settlement of regional disputes under the principles of non-interference and decision making through consensus, also known as the ‘ASEAN Way’.4 Right from the start, the Association embraced the different political construct existing amongst its member nations. This in a way has helped the association address issues such as the confrontation between Malaysia and Indonesia during the 1960s as well as helped lessen tensions among Malaysia, Indonesia, and the Philippines over Borneo.5

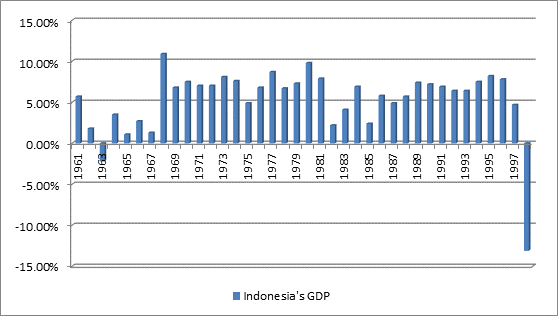

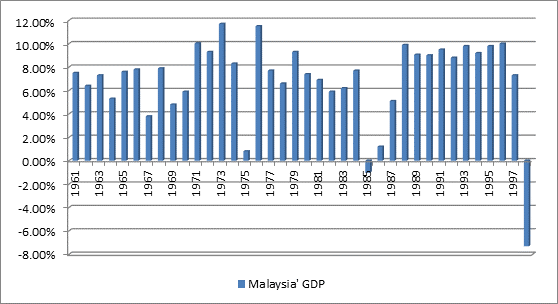

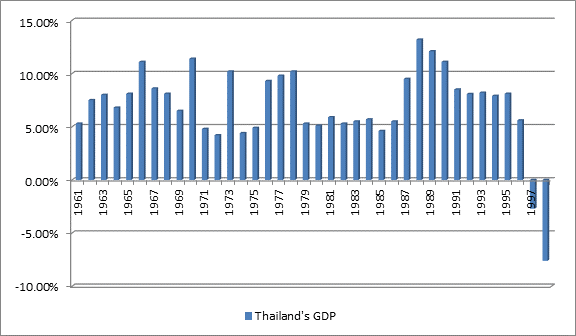

A relatively stable regional atmosphere made it possible for member-states to put all their resources and efforts into the goal of nation-building and economic development. Many of the ASEAN states inspired by Japan’s industrialisation of the late nineteenth century and then its rapid recovery following the World War II began adopting a policy of ‘Look East’. They mixed form of capitalism along with a activist government, helped spur economic growth resulting in ASEAN countries such as Indonesia, Malaysia, Singapore, and Thailand gaining the reputations as ‘tigers’ in the 1980s because of their economic dynamism. The government in these nations even though pushed development through a market based economic system, played its role by stimulating trade and growth and maintained an authoritarian political system to ensure social stability.6 The following bar diagrams indicates the GDP of these four ASEAN states namely; Indonesia, Malaysia, Singapore, and Thailand from 1961 till the year following the Asian financial crisis of 1997.

Figure One: Indonesia’s GDP, 1961-1998 (in percentage)7

Figure Two: Malaysia’s GDP, 1961-1998 (in percentage)8

Figure Three: Singapore’s GDP, 1961-1998 (in percentage)9

Figure Four: Thailand’s GDP, 1961-1998 (in percentage)10

The four ASEAN member states as indicated in the bar diagram witnessed rapid economic growth from the 1960s onwards, with Singapore and Malaysia reaching GDP growth of more than 13 and 10 percent respectively. This sustained high GDP growth helped Southeast Asia emerge as an attractive destination for foreign investment and labour migration into the fast developing states of Malaysia, Singapore, and Thailand. After a dismal growth in the 1960s; under President Suharto (1967-1998) Indonesia’s economic growth began to grow between 6 to 10 percent as indicated in figure one. Suharto was keen on creating a modern economy with strong hand of the government. Moving from Sukarno’s ‘Guided Democracy’, Suharto’s ‘New Order’ was based on the premise of modernity. This new approach attracted multinational corporations into its market that helped turn Indonesia into an exporter of manufactured goods.11

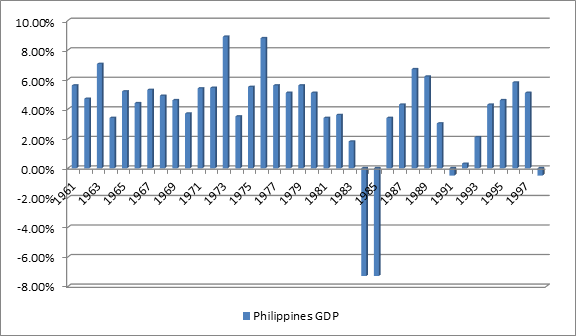

Figure Five: Philippines GDP 1961-1998(in percentage)12

Philippines which had enjoyed one of the most robust economies before World War II lagged behind the other four ASEAN states partly due to its unstable political environment. Its GDP from 1961 onwards projected in figure five indicates that unlike the other four ASEAN states it had a comparatively moderate growth with a negative growth of -7.3 percent in 1984 and 1985. During the Presidency of Ferdinand Marcos (1965-1986), martial law was imposed from 1972 till 1981. This not only challenged the political democracy in the Philippines but also impacted its economic growth. Further, the oil shocks of 1973 and 1979 raised import prices dramatically and destabilised export prices. Between 1979 and 1983 Philippines foreign debt doubled along with increasing inflationary pressure at home. Maria Corazon Aquino, who took over the presidency on February 1986, had a reformist, market-focused, and internationally orientated approach. Given that Philippines was so deeply in debt it needed to participate in the global economy by aligning itself with the rest of Southeast Asian nations, who at that time were moving towards globalisation.13 The adoption of market-based economy with a heavy hand of the government in most of the ASEAN member states in the early years, helped millions experience rising living standards. This made Southeast Asia one of the most attractive markets for investors and labours, until the Asian monetary crisis hit the region in 1997.

ASEAN in the Post- Financial Crisis Era

In the aftermath of the Asian financial crisis, in all of the ASEAN states growth declined to settle in the negative. At this point the ASEAN Free Trade Agreement (AFTA) had already been signed in January 1992. Further, from the original five countries which included Thailand, Indonesia, the Philippines, Singapore, and Malaysia, the association had expanded its membership to include Brunei (1984), Vietnam (1995), Myanmar (1997), Laos (1997), and Cambodia (1999). The financial crisis of 1997 took place in an era of rapid globalisation, that witnessed major role being played by international bodies such as the World Trade Organisation, the International Monetary Fund, and the World Bank. These organisations established and enforced the rules of globalisation to which nations in Southeast Asia were part of. Southeast Asian governments were asked to liberalise their financial markets, puttting an end to many restrictions that formerly regulated the flow of capital into and out of their countries. This integration through globalisation saw the growth of joint ventures and foreign-financed enterprises, leading to a double-digit economic growth and trade balances in most of the ASEAN states.14

Given that Southeast Asia provided multinational enterprises with low factor cost maunfacturing platforms. Between 1980 and 1996, when the stock of world FDI increased from about US $ 514 billion to around US $ 3,233 billion; Southeast Asia’s share rose from 6.7 percent of the total to 14.7 percent. According to UNCTAD report of 1997, although ASEAN’s share of developing country FDI stock declined from 71 percent of total in 1980 to 42 percent of the total in 1996, its FDI inflows as a share of in-FDI to developing countries nearly doubled from 29.8 percent of total in 1980 to 51.9 percent of total in 1996. Furthermore, of the US$ 256 billion FDI inflows to developing countries US $ 90 billion went to Southeast Asia. Thus, FDI in ASEAN rose over six-fold since 1980 and by two-thirds since 1990.15

The nations in Southeast Asia had to face the onslaught of the financial crisis that had a ripple effect across the region, pushing down their growth the following year. The 1997 Asian financial crisis shook Southeast Asia’s confidence in open trade and financial globalisation. Paul Krugman in a 1994 paper published in Foreign Affairs titled, ‘The Myth of Asia’s Miracle’, argued that the growth in Asian Countries was mainly triggered by the increase in labour input without achieving technological development. According to Krugman the remarkable economic growth in Southeast Asia since the 1980s could be very much compared to the experiences of most Eastern European countries which also faced collapse at the end of the 1980s. The growth achieved by most of the Southeast Asian countries in the beginning of the 1990s was in the absence of any fundamental increase in its labour productivity.16 Further, the market failure arising out of the dilemma of attempting to maintain simultaneous capital account liberalization, fixed exchange rates and independent domestic monetary policy, snowballed into a full fledged economic crisis throughout the region.17

In December 1998 at the ASEAN+ 3 Summit (ASEAN member states plus China, Japan, and South Korea) held in Hanoi, China proposed to establish the ASEAN+ 3 Finance Ministers’ Deputies’ Meeting (FMDM), which held its first meeting in March 1999. The third ASEAN+ 3 Summit held in November 1999 in Manila saw the adoption of a ‘Joint Statement on East Asia Cooperation’, which laid the ground work for the establishment of financial regionalism in East Asia through the ASEAN+ 3 framework. Through this Chiang Mai Initiative (CMI) was established in May 2000, with provisions of short term financing facilities of US $ 15 billion that aimed to provide liquidity to Asian countries, to avoid balance of payment problems. Further, long term facilities of US $ 15 billion was also made avaliable for the reconstruction of crisis-hit economies.18

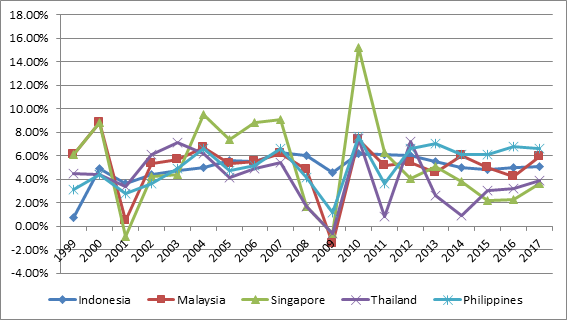

Figure Six: GDP of Indonesia, Malaysia, Singapore, Thailand and Philippines, 1999-2017 (in percentage)19

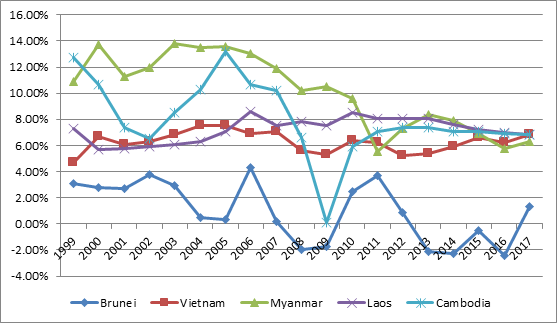

Figure Seven: GDP of Brunei, Vietnam, Myanmar, Laos, and Cambodia, 1999-2017 (in percentage)20

To a significant degree, the crisis set Southeast Asian countries into a slower growth trajectory that persist till date. The line graphs in Figure Six and Seven indicates the GDP of the ASEAN member states in the post Asian financial crisis period. Amongst the original ASEAN member countries, barring Singapore which achieved a GDP between 6 to a high of 15.2 percent in 2010, the average growth remained between 5 to 6 percent. The other ASEAN countries barring Brunei witnessed a higher growth, with their current average growth being in the range of 6 to 7 percent.

Towards the ASEAN Economic Community

The ASEAN Economic Community Blueprint 2025, adopted by the ASEAN Leaders at the 27th ASEAN Summit on November 22, 2015, in Kuala Lumpur, identifies the realisation of the AEC as the end goal of ASEAN’s economic integration. It envisions ASEAN as a single market and production base, a highly competitive region, with equitable economic development, and fully integrated into the global economy. The establishment of the AEC would allow for the free movement of goods, services, and investments as well as freer flow of capital and skills; transforming the entire region into a single investment destination.21 In the aftermath of the Asian financial crisis which had derailed Southeast Asia’s economic growth. Security challenges in the new millennium, from terrorism in the post 9/11 era to issues in the contested South China Sea to an unstable nuclear Korean Peninsula to the ongoing ethnic violence in some parts of Southeast Asia. These factors causes as an impediment to the free flow of trade and commerce. The current uncertainty to the existing open and rules-based multilateral trading system – which has for long underpinned the region's economic growth – further add to the concerns, as it becomes detrimental towards the realisation of the AEC.

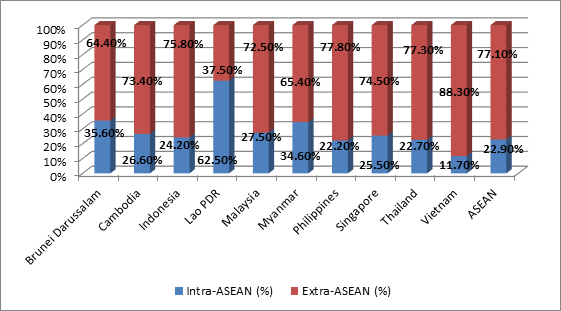

However, in spite of these emerging concerns and challenges, ASEAN is expected to remain resilient and maintain a steady growth path, given the prevalence of strong economic fundamentals in the region. According to the ASEAN Economic Integration Brief, June 2018, the region’s economy grew 5.3 percent in 2017 with GDP at Current Price at US $ 2,765.7 billion and GDP per Capita at US $ 4,305 billion. For 2018 and 2019 the growth is forecast at 5.2 percent, driven by private consumption, strong investments particularly in public infrastructure and exports. ASEAN’s total trade also grew by 14.2 percent year-on-year to US $ 2.6 trillion in 2017. The following bar diagram in Figure Eight indicate the Intra-ASEAN and Extra-ASEAN total trade in goods for 2017. The figure indicates the overdependence of ASEAN member states on external trade which in 2017 was 77.1 percent of its total trade in goods. Individually as well all the ASEAN countries have a higher proportion of their trade outside the region.22

Figure Eight: ASEAN’s Intra and Extra Trade in Goods, 2017 (in percentage)23

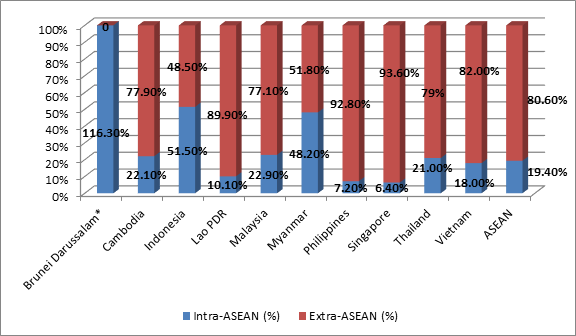

Further, there has also been a strong inflow of FDI into the region, increasing by 11.6 percent year-on-year to reach US$ 137 billion at the end of 2017. The following bar diagram indicate the total FDI inflows into ASEAN and its ten member states in 2017. From the data in the figure it is evident that 80.6 percent of the FDI inflows continue to come from outside ASEAN while the remaining 19.4 percent is intra-ASEAN. Indonesia and Brunei are the only two ASEAN countries which received majority of its FDI inflows from within ASEAN. Countries such as Singapore, and the Philippines, receive more than 90 percent of their FDI inflows from outside ASEAN.

i * indicates minus or decrease of 16.3%

Figure Nine: Intra and Extra-ASEAN Investment, 2017 (in percentage)24

Regionalism has today become an important feature of the global trading system, and for ASEAN it continues to remain its core. ASEAN is engaged in promoting the continuity of a multilateral open and free trade order, integral for its sustenance and growth. For instance, although the US comprises only US $ 1.1 billion or 6 percent of ASEAN’s total trade in aluminium, the 10 percent tariff imposed by the Trump administration in 2018 on aluminium products will leave a dent, considering that the US is ASEAN’s second largest aluminium export destination with US $ 0.8 billion after Japan with US $ 1.0 billion.25

Further, to overcome the various limitations ASEAN is also pushing major connectivity initiative provided by its ‘Master Plan on ASEAN Connectivity 2025’. This would help complement growth and held achieve a seamlessly and comprehensively connected ASEAN that will promote competitiveness, inclusiveness, and a greater sense of community.26 During the meeting of the International Monetary Fund (IMF) and World Bank held on October 12, 2018, in Bali, the ASEAN leaders reiterated their commitment towards upholding the open and rules-based multilateral trading system. Singapore's Prime Minister Lee Hsien Loong also stated that ASEAN is redoubling its efforts on the Regional Comprehensive Economic Partnership (RCEP), and hopes to achieve a "substantial conclusion" by the year-end.27

The ongoing RCEP negotiations between ASEAN and Australia, China, India, Japan, South Korea, and New Zealand; once concluded would make it the world’s largest economic block, covering nearly half of the global economy and 3.4 billion people. The Ministers from the 16 RCEP Participating Countries (RPCs) while attending the 6th RCEP Inter-Sessional Ministerial Meeting held on October 13, 2018, in Singapore reaffirmed their resolve to bring negotiations to a substantial conclusion particularly at the time of uncertainties in global trade.28

Thus, ASEAN while continuing to promote regional stability through economic cooperation is doing so with the intent of establishing an integrated economic community which would be crucial for the overall long term development and growth of the region. With the establishment of a free trade agreement in 1992 today the ASEAN trade block has become one of the largest in the world. Further, with the conclusion of the RCEP negotiation and once fully realised it would become a major milestone, particularly at a time of uncertainties to the existing multilateral trading order. This would also ensure the centrality and unity of ASEAN which would be crucial going forward towards establishing an economic community.

Conclusion

ASEAN unlike the European Union (EU) did not have the advantage of being well-endowed in terms of resources and development along with a shared religious culture and a common legal heritage. Having completed 50 years in 2017, ASEAN by embracing half a billion people that make up the region and by adopting the principle of non-interference and decision making through consensus, it has helped it to become one of the most successful regional organisations in the non-Western world.29 ASEAN has not attained the level of sophistication as exhibited by the European Union. However, as the Association continues to push its integration process while ensuring equitable economic growth amongst all its member- state, the establishment of a Union seems to be on track. The establishing of the AEC which is crucial to its ongoing integration process needs to overcome challenges such as the current pressure to the multilateral trading system. It must be realised that ASEAN after the financial crisis of 1997 has made the necessary correction and today its economic fundamentals seems strong and stable, as evident by the increase in its investment inflow. The ongoing tariff barriers from the US and the import reduction on items such as palm oil by the EU which intents to phase out the use of bio-fuel as transport fuels from 2030, are no doubt areas of concern. Thus, it is crucial for ASEAN to remain resilient and continuously innovate in order to overcome these pressures, while moving towards the AEC.

***

* The Author, Research Fellow, Indian Council of World Affairs, New Delhi.

Disclaimer: The views expressed are that of the Researcher and not of the Council.

Endnotes

1 “Joint Communiqué of the 51st ASEAN Foreign Ministers’ Meeting Singapore”, ASEAN, August 2, 2018, http://asean.org/storage/2018/08/51st-AMM-Joint-Communique-Final.pdf, accessed on August 8, 2018.

2 “ASEAN must stay the course and press on with economic integration and innovation: PM Lee”, The Straits Times, August 2, 2018, https://www.straitstimes.com/politics/asean-must-stay-the-course-and-press-on-with-economic-integration-and-innovation-pm-lee, accessed on August 2, 2018.

3 “ASEAN Economic Integration Brief no.03/ June 2018”, ASEAN, http://asean.org/storage/2018/02/AEIB_3rd-Issue_v3-Ready-Print-Single-Page.pdf, accessed on July 16, 2018.

4Kristoffer Daniel Li, “The Point of ASEAN”, The Diplomat, July 30, 2016, https://thediplomat.com/2016/07/the-point-of-asean/, accessed on November 2, 2018.

5Norman G. Owen (Edi), The Emergence of Modern Southeast Asia: A New History, (University of Hawai`i Press: Honolulu, 2005), p. 396-397.

6 Craig A. Lockkard, Southeast Asia in World History, (Oxford University Press: New York, 2009), p. 170-171.

7See:https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?end=2017&locations=ID&start=1961&view=chart, accessed on October 10, 2018.

8See:https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?end=2017&locations=MY&start=1961&view=chart, accessed on October 10, 2018.

9See:https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?end=2017&locations=SG&start=1961&view=chart, accessed on October 10, 2018.

10See:https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?end=2017&locations=TH&start=1961&view=chart, accessed on October 10, 2018.

11Norman G. Owen (Edi), The Emergence of Modern Southeast Asia: A New History, (University of Hawai`i Press: Honolulu, 2005), p. 435-438.

12See: https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?locations=PH, accessed on October 11, 2018.

13 Norman G. Owen (Edi), The Emergence of Modern Southeast Asia: A New History, (University of Hawai`i Press: Honolulu, 2005), p.455-463.

14 Robert Dayley and Clark D. Neher, Southeast Asia in the New International Era, (Westview Press: Colorado, 2013), p. 12- 13, and 17

15 Frank L. Bartels and Hafiz Mirza, “The Asian Crisis- Signals from Multinational Enterprises: Obstacles and Managerial Impediments to Foreign Direct Investment”, in Partha Gangopadhyay and Manas Chatterji (edi), Economic Globalisation in Asia, (Ashgate Publishing Limited: Hampshire, 2005), p.24-25.

16 Chang Woon Nam, “Major Causes of the Korean and Asian Economic Crisis”, in Partha Gangopadhyay and Manas Chatterji (edi), Economic Globalisation in Asia, (Ashgate Publishing Limited: Hampshire, 2005), p. 90-91.

17Frank L. Bartels and Hafiz Mirza, “The Asian Crisis- Signals from Multinational Enterprises: Obstacles and Managerial Impediments to Foreign Direct Investment”, in Partha Gangopadhyay and Manas Chatterji (edi), Economic Globalisation in Asia, (Ashgate Publishing Limited: Hampshire, 2005), p.25.

18Shintaro Hamanaka, Asian Regionalism and Japan: The politics of membership in regional diplomatic, financial and trade groups, (Routledge: Oxon, 2009), p. 117-118.

19 See No 6, 7, 8, 9 and 11.

20See:https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?locations=BN, https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?locations=VN, https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?locations=MM, https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?locations=LA, https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?locations=KH, accessed on October 11, 2018.

21“ASEAN Economic Community”, ASEAN, https://asean.org/asean-economic-community/, accessed on October 25, 2018.

22“ASEAN Economic Integration Brief no.03/ June 2018”, ASEAN, http://asean.org/storage/2018/02/AEIB_3rd-Issue_v3-Ready-Print-Single-Page.pdf, accessed on July 16, 2018.

23 Ibid.

24 Ibid.

25 Ibid.

26 “Joint Communiqué of the 51st ASEAN Foreign Ministers’ Meeting Singapore”, ASEAN, August 2, 2018, http://asean.org/storage/2018/08/51st-AMM-Joint-Communique-Final.pdf, accessed on August 8, 2018.

27 Nur Asyiqin Mohamad Salleh, “ASEAN leaders vow to uphold multilateral trade system”, The Straits Times, October 12, 2018, https://www.straitstimes.com/asia/se-asia/asean-leaders-vow-to-uphold-multilateral-trade-system, accessed on October 12, 2018.

28“The 6th Regional Comprehensive Economic Partnership (RCEP) Intersessional Ministerial Meeting 13 October 2018, Singapore”, ASEAN, https://asean.org/storage/2018/10/RCEP-ISSL-MM-6-JMS-FINAL.pdf, accessed on October 15, 2018.

29 Norman G. Owen (Edi), The Emergence of Modern Southeast Asia: A New History, (University of Hawai`i Press: Honolulu, 2005), p. 396-397.